Quick and Friendly Loans Even With Bad Credit

Quick and Friendly Loans – this financial website shows various quick loans and credit offers to bring you financial products or services for you to view as part of our friendly loan services.

The owner of this website has been in the finance industry since the year 2000 and has a lot of experience in both unsecured and secured lending.

Get Same-Day Approval with a Simple, Secure Online Application. No Hidden Fees. No Stress!

The main products you can apply for on this website are Personal Loans, Car Loans, Secured Homeowner Loans and Mortgages a new bank account and various other types of credit.

All products are suitable to apply for if you either have a crystal clear credit history or have some bad credit.

Decisions in Minutes From Approved UK Lenders – Get a Quotation Here:

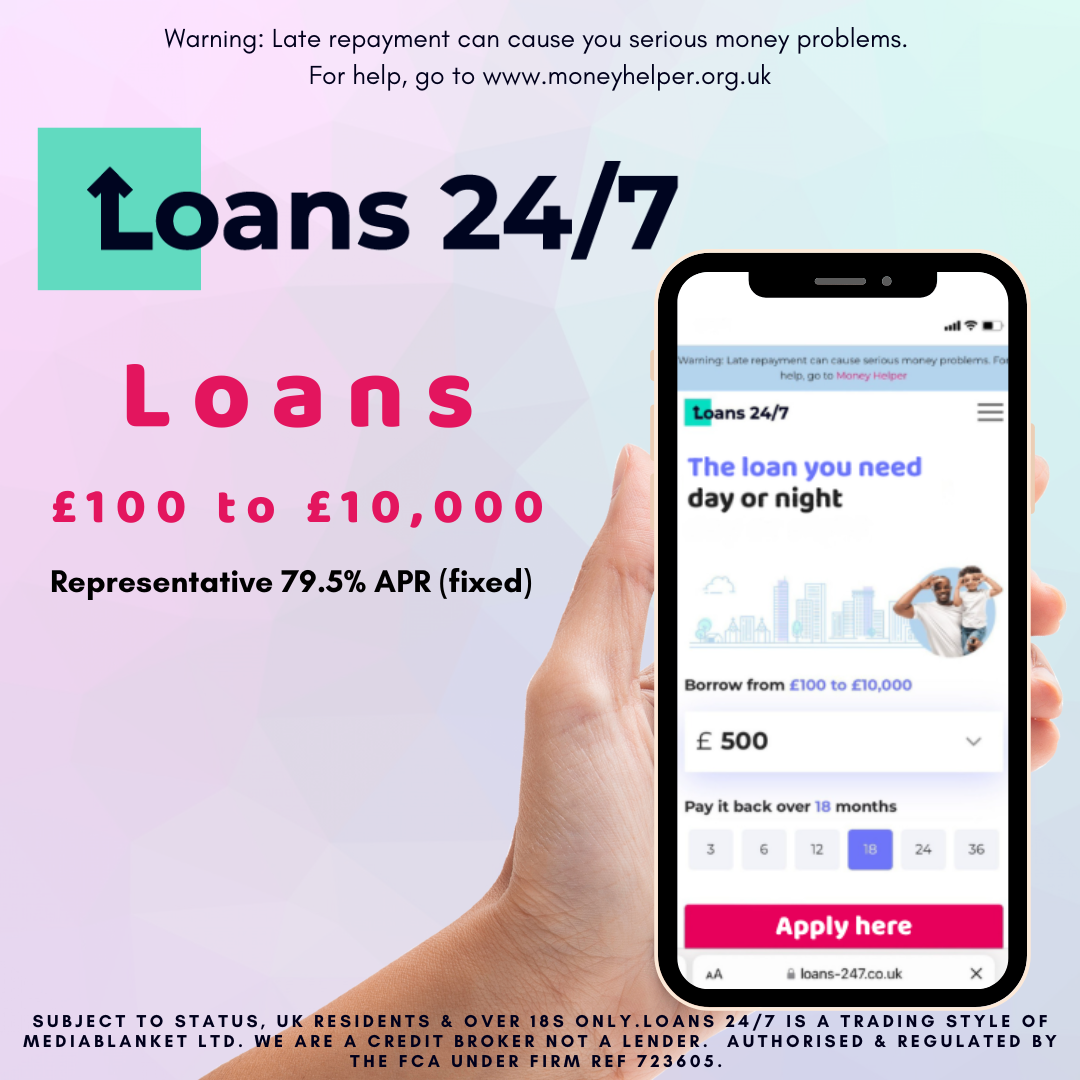

Sponsored:

Are you in need of a quick financial solution in the UK? Look no further than Quick and Friendly Loans Limited! With their speedy and friendly service, they are your go-to partner for all your loan needs. Let’s explore why they are the best choice for anyone looking for a fast and easy loan in the UK.

Fast, Friendly Loans – Even with Bad Credit

Get same-day approval with a simple, secure online application. No hidden fees. No stress.

Apply in 2 minutes

Check Your Eligibility

Why Choose Quick and Friendly Loans?

- ✅ Quick Approvals – Most applications are processed within minutes

- ✅ All Credit Scores Welcome – We help people with poor or no credit

- ✅ Transparent & Secure – No hidden fees. Your data is 100% protected

- ✅ UK-Based, Trusted Since 2012 – Trusted by thousands across the UK

“The process was simple and fast—I had the money the same day!” – ★★★★★ Heather S.

How It Works

- Apply Online: Use our simple form to apply in under 2 minutes.

- Get a Quick Decision: We match you with a trusted lender and send you a quick response.

- Receive Your Funds: Once approved, funds are transferred—often the same day.

Real People. Real Help.

Need help or have questions? Our UK-based support team is ready to assist you—just reach out via email. We believe in real, friendly service—no bots, no jargon.

Loan Options We Offer

- Same-Day Loans

- Bad Credit Loans

- Short-Term Loans

- Payday Loans

- Personal Loans

- Car Loans

- Secured Homeowner Loans

Safe, Secure & Registered

We are a credit broker, not a lender. That means we work with a trusted network of FCA-authorized lenders to find you the best deal. Your data is encrypted and handled with care. This website is secure and has the “https” prefix for security.

The Fastest Way to Get a Loan in the UK

When it comes to getting a loan, time is of the essence. Quick & Friendly Loans Limited understands this, which is why they offer the fastest loan processing in the UK. With their simple application process and quick approval times, you can have the money you need in your account in no time. Say goodbye to long waits and tedious paperwork – Quick & Friendly Loans Limited has got you covered!

Friendly Loans: Your Financial Lifesaver!

Not only is Quick & Friendly Loans Limited fast, but they are also friendly and reliable. Their team of loan experts is always ready to assist you with any questions or concerns you may have. Whether you need a small loan for a personal expense or a larger loan for a business venture, they will work with you to find the best solution for your needs. With Quick & Friendly Loans Limited, you can rest assured that you are in good hands.

Quick and Easy Loans Limited: Your Trusted Partner

Quick & Friendly Loans Limited is not just a loan provider – they are your trusted partner in financial success. With their transparent terms and competitive rates, you can feel confident in your decision to choose them for your loan needs. Whether you have good credit, bad credit, or no credit at all, Quick & Friendly Loans Limited will work with you to find a solution that fits your unique situation. Say goodbye to financial stress and hello to peace of mind with Quick & Friendly Loans Limited by your side.

Don’t let financial worries weigh you down – choose Quick & Friendly Loans Limited for all your loan needs and experience the fast and friendly service you deserve. With their quick processing times, friendly customer service, and trusted reputation, you can’t go wrong. Say goodbye to financial stress and hello to financial freedom with Quick & Friendly Loans Limited today!

Quick and Friendly Loans – Legal Stuff

Please ensure you read through all of the terms and conditions of any loan offer you may be made, including the loan amount, repayment period, interest rate used, etc. and only if you are happy, you may proceed to accept the new loan offer online.

For more information on how we handle your data see our Privacy Policy which has links to our Terms and Conditions, Cookie Policy, our policy on Responsible Lending and how we handle and deal with Making Complaints.

More…

Please feel free to use the Quick & Friendly Loans Contact page for any items you want to bring to our attention, including a recommendation if you feel we got it right. You can view all the Pages and Posts on this website and also any Financial News.

If you have any questions or queries regarding Quick & Friendly Loans, you might like to visit our frequently asked questions page first or find out what we are About.

Warning: Late repayment can cause serious money problems. For help, go to Money Helper