What is the Best Way to Finance a Car?

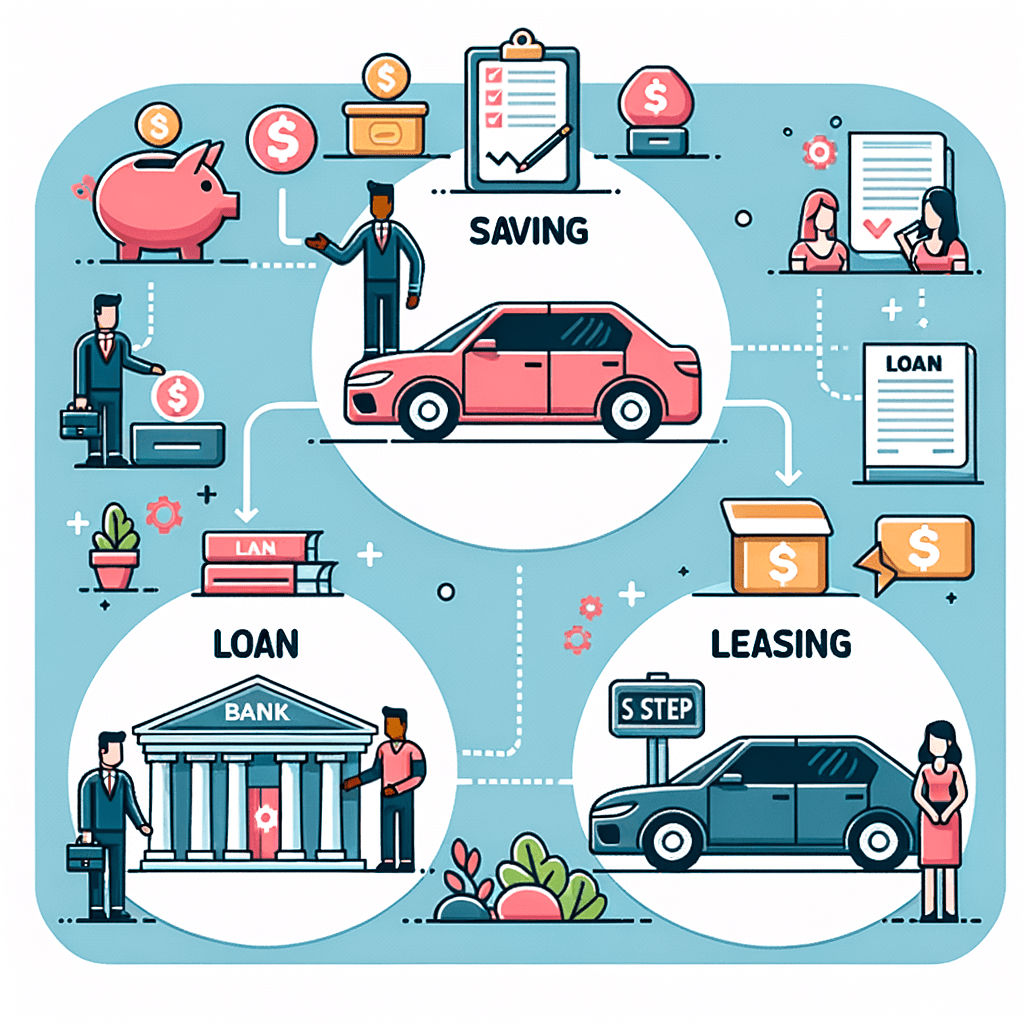

Best Way to Finance a Car – there are several ways to finance a new or used car. While you can save up for the purchase, preapproval and leasing may be the best way to go.

Here are some tips on how to get preapproved. Leasing a vehicle is not a good idea if you don’t have a lot of money. Shopping around for a loan through a direct lender will help you find the best deal.

Pre-approval

While getting preapproved isn’t always necessary, it is beneficial because it gives you more negotiating power when you meet with a dealer.

You can even negotiate lower interest rates with the dealer if he or she offers a lower rate than the one you have preapproved. Getting preapproved can be an excellent way to finance a new or used car, especially if you want to finance the entire purchase.

Before you begin your search, take your preapproval letter to the dealership. You will want to browse a wide variety of vehicles and stick with those that fit within your budget.

After you find the perfect car, complete your application. Some lenders have limitations on the types of vehicles they will finance, primarily based on the age and mileage of the vehicle. By preapproval, you can save time and hassle when applying for financing.

Recommended Reading

Leasing

There are many benefits of leasing a car, including a lower monthly payment. While leasing is generally less expensive than buying, it is also subject to restrictions.

In order to avoid lease limitations, you should first do your research and visit a few dealerships before making your decision. Call ahead to find out when you can take a test drive and what kind of policies they have.

Lastly, you should expect to pay a higher price for your car on dealer lots. However, even though the inventory shortage has affected the car finance leasing market, overall it is still cheaper than buying a new or used car.

Leasing is not the best way to finance a car loan. Although you will own the car, you may have to return it in great condition, which isn’t always possible.

Moreover, you may end up paying more in maintenance costs and repair costs when your lease expires. You can also use an auto loan calculator to find the best interest rate and loan terms. If you’re not sure which option is best for you, try using a car loan calculator.

Saving up

If you have extra money lying around and you don’t know what to do with it, the first option is saving up for a car loan. It sounds obvious, but it can actually help you become debt free.

A new car costs on average £32,187, while a used car costs around £20,137. With extra money you save up for a car loan, you can afford to pay off the loan, and you can even drive the new car for free!

If you’re buying a new car, it’s a good idea to save up for a down payment of at least 10%. In addition, you should aim for a down payment of 20% or more if you’re going for a used car.

For example, a used car will usually require a down payment of £2,000, while a new one will cost you £30,000. If you’re planning on financing the car, make sure to set aside a small percentage of your income every month for a down payment.

Getting a loan with a low interest rate

When looking for a car loan, you want to get the best interest rate possible. But even though a lower interest rate will ultimately save you money, fees and other costs will add up.

So, how can you get a lower interest rate? To get a low rate, improve your credit score. This process may take a few months or even a year, but it will definitely help your credit score and lower your overall auto loan cost.

One easy way to improve your credit score is to make on-time payments and keep your balances low on your credit cards.

Whether you are looking for a new car or a used one, you should shop around for the lowest interest rate possible. Before applying for a loan, compare loan rates from different lenders.

Getting pre-approval will put you in a better negotiating position and help you avoid being turned down by the lender. It will also give you some leverage when negotiating with the dealership. When negotiating for a car loan, it is best to bring your pre-approved letter from your bank with you.

Best Way to Finance a Car