How to Get Unsecured Personal Loans With Unreliable Credit History

How to Get Unsecured Personal Loans With Unreliable Credit History – If you have poor credit, you may be wondering how to get unsecured personal loans with bad credit.

The good news is that obtaining unsecured loans does not have to be a difficult process. While your credit score will play a huge role in the decision, you should also understand that having a poor credit score will make your options much more limited.

While you will have fewer choices and pay higher interest rates, obtaining an unsecured loan with bad credit is still possible.

To learn more about the trade-offs and the various types of unsecured personal loans, you can begin your search for the right one for your circumstances.

Payday loans are unsecured loans with unreliable credit history

A payday loan is a short-term unsecured loan that requires a check, or permission to electronically withdraw money from your bank account.

The money is due on your next pay day, typically in two weeks, but may be due as late as a month. Payday loans issued in a store will require you to return on your due date to pay them back.

Recommended Reading

The lender will run a check and make an electronic withdrawal for the amount of the loan, plus interest. Payday loans issued online use electronic withdrawal instead.

While payday loans may seem like a good option for those with less-than-stellar credit, they can be problematic. Although they are quick and easy to apply for, they are often unsecured, which means that your credit history can play a factor.

Moreover, these loans are often difficult to get, unless you have reasonable credit. Because of their high interest rates, they are often referred to as predatory. But in reality, payday loans can be a great solution for those who need cash fast but have less-than-stellar credit history.

Unsecured loans don’t require collateral

When you have bad credit, it can be difficult to qualify for personal loans. Fortunately, this is not the end of the world.

There are many lenders willing to help people with bad credit get the money they need. You can search online or in brick-and-mortar banks for unsecured personal loans.

Either way, it’s important to know your options. While unsecured personal loans are not standard loans, they do have favourable interest rates.

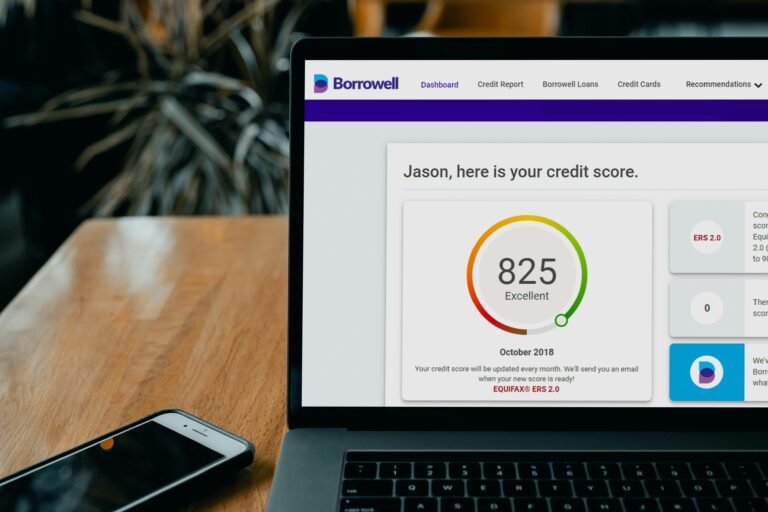

The primary difference between secured and unsecured loans is their impact on your credit score. When you apply for a loan, lenders will check your credit report any negative information to the two major consumer credit bureaus.

These companies report information to the two credit bureaus: Equifax and Experian. You need to pay attention to these credit reports because the lenders can use them to check your payment history and determine if you are a good candidate.

Unsecured Loans No Guarantor Bad Credit

Higher interest rates

As the name suggests, unsecured personal loans with an unreliable credit history come with higher interest rates. The longer the repayment terms, the higher the interest rate.

This is not an issue for those with a good credit score, since most lenders offer longer repayment terms than borrowers with bad credit. However, borrowers with bad credit may face higher interest rates, and they should consider other options such as 0% balance transfer credit cards.

Unsecured personal loans with unreliable credit history are difficult to qualify for, because lenders look at the payment history on your credit report.

While these loans have strict terms, they are a good alternative if you’re in a pinch. For example, you can find a personal loan with a high interest rate if you have a 720-credit-score and are seeking funds for an emergency or an unexpected expense.

Less favorable terms

When looking for unsecured personal loans, the first thing you should remember is that your credit score is the most important factor in determining your loan amount and interest rate.

In fact, if you have an excellent credit score, you can often get the lowest rates and maximum loan amounts. On the other hand, if your credit history is less than perfect, you will likely end up getting the highest rates and terms.

Lenders also consider your length of credit history. Most of them will require that you have had at least two years of credit history before they can approve you. The longer your credit history, the better.

How to Get Unsecured Personal Loans With Unreliable Credit History